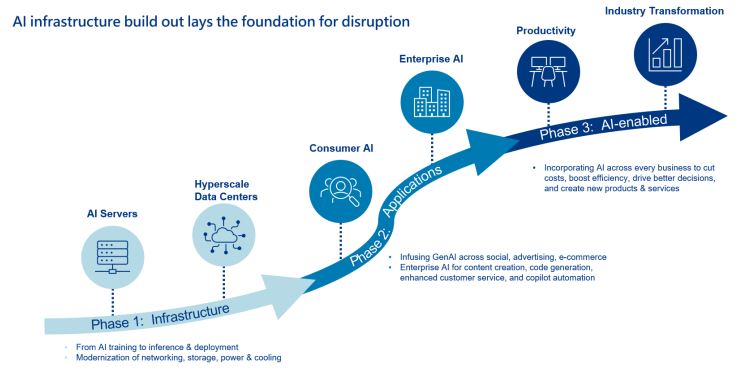

Roadmap of the Upcoming AI Innovation Wave

Global equity markets cleared the half-way point of 2024 on a strong note. Markets were remarkably resilient against a backdrop where inflation moved sideways during the year, prompting the federal reserve to maintain its restrictive stance. This caused a shift in rate cut expectations for calendar year 2024, as markets priced in six rate cuts at the beginning of the year and expectations are now for approximately two cuts. Although such a backdrop is typically a headwind for equities, strong corporate earnings results and confidence in forward expectations helped the stock market extend its rally from 2023 into this year.

With markets near all-time-highs, the S&P 500 currently trades at a price-to-earnings of 21x, which is slightly above its most recent 5-year average. Valuations can remain elevated for longer periods, especially for companies in growth-oriented industries, as markets expect higher earnings to grow into their valuation. We expect this trend to continue, especially for companies that are aligned to the ongoing AI innovative wave.

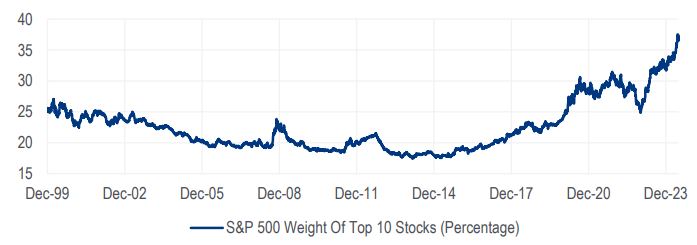

However, a key characteristic of this equity rally is that returns are concentrated among a handful of large technology companies. Many market commentators pointed to the narrow market leadership to conclude that the rally is unsustainable, as the top 10 stocks in the S&P 500 account reached a multi-decade high of 37% of the index. However, we argue that investors are misunderstanding the nature and implication of this market concentration.

S&P 500: Weight of Top 10 Stocks

To clarify, the narrow market leadership is largely a function of the AI industry structure. Over the last several years, the large technology giants have heavily invested in their AI capabilities in the form of infrastructure and solutions, including large accelerated computing clusters for AI training. These tech giants are natural beneficiaries amid the generative AI innovation wave.

It is worth highlighting that excitement surrounding the AI Infrastructure buildout continues to be scrutinized by investors, with a fair amount of skepticism on the durability of the investment cycle. In this environment, AI companies that have demonstrated earnings outperformance and good visibility on growth have been rewarded by investors while those AI companies that have exhibited near-to-intermediate term softness and mixed outlooks have been punished by the market. From an IPO perspective, public equity investors demand companies that can deliver revenue growth with profitability, a challenging threshold for many pre-IPO companies. There is a lack of euphoria that is typically associated with past hype cycles, and we see a growing pipeline of exciting private AI companies that could come public in the next few years.

As for what’s next, we expect the capital investments surrounding the “Phase 1” AI Infrastructure to remain strong, but the risk-reward has become more balanced after recent the strong performance. Even within AI Infrastructure, we are seeing a broadening beyond GPU chip companies to other areas that includes cyclical semiconductors, hardware providers and even power related companies. Moreover, we believe the generative AI Innovation wave is likely entering “Phase 2”, which should demonstrate more use cases and adoption in AI Applications. This is a similar pattern to past technology innovation cycles, as a proliferation of new software products and solutions was a direct result of the infrastructure buildout. We are also seeing early signs of “Phase 3” emerge with as new industry leaders demonstrate the effective use of generative AI.

Source: Piper Sandler

The AI Innovation Cycle: Early days in the AI innovation journey

The transition from phase 1 to phase 2 will be catalysed as new generative AI applications move from pilots into production. From our conversations with infrastructure software & services related companies, there is a growing pipeline of AI applications under development across the enterprise and consumer. Software and service providers are beginning to rollout new generative AI capabilities to drive greater value and create additional monetization opportunities. Early innovations around content creation, code generation and co-pilots look promising. On the consumer side, we continue to see an infusion of AI capabilities across social media, e-commerce and advertising. It is worth highlighting that Apple, a previously considered an AI laggard, made their “Apple Intelligence” announcements during its Worldwide Developers Conference in June of this year. The event marks a potential turning point, as Apple is focused on enabling developers create new AI capabilities that can interface with Apple’s installed base of over 2.2 billion users. Big picture, we believe that heading into 2025 and beyond, the current set-up likely leads to a Cambrian explosion of AI-integrated applications. The investment potential remains attractive, as the growth potential has been largely underappreciated by investors.

Review of Allianz Global Artificial Intelligence

Over the year-to-date period as of June 30, 2024, the Allianz Global Artificial Intelligence Fund underperformed on a net-of-fees basis versus the custom benchmark (50% MSCI ACWI Index/50% MSCI World Information Technology Index). Relative performance headwinds can be isolated to two key factors: extremely narrow market leadership and underperformance within AI Applications. Both of these factors represent short-term headwinds but longer-term opportunities. Also, some stock-specific underperformance also weighed on returns.

A Narrow, but Misunderstood Market

Our custom benchmark has grown to become even more concentrated than the broader market indices, such as the S&P 500 or MSCI ACWI. The top three positions have grown to represent 33% of the custom benchmark at the end of the most recent quarter. An underweight to names like NVIDIA was a headwind to relative returns year-to-date. A reminder that the Allianz Global Artificial Intelligence Fund is a diversified strategy and is not managed relative to a benchmark and typically has high active share. By design, we will be structurally underweight to excessively large positions in the benchmark.

Moreover, such a concentration represents a key risk for strategies that strictly track equity indices. In the last two calendar years, the mega-cap technology companies exhibited relatively better earnings resiliency and growth. However, a cautious eye is warranted when their earnings growth begins to slow compared to other areas in the publicly traded equity universe. A backdrop of other companies emerging as AI beneficiaries and investors underappreciating their potential creates an opportunity for stock selection in a potential market broadening environment. Central banks are leaning towards an eventual easing in monetary policy. Amid a resilient economy, this scenario is constructive for a broadening in markets across sectors. The overall backdrop points to better risk-reward opportunities outside the mega-cap technology space as we look forward.

An Underappreciated Stock Selection Opportunity within AI Applications

Over the first half of the year, AI Applications represented a key performance headwind for the fund, as these companies faced headwinds from tighter IT budgets, some crowding out effect from robust AI infrastructure spending, and pause waiting to see new generative AI features. Despite the near-term underperformance, we still believe that we are early to the upcoming inflection point for AI Applications. A lot of negative sentiment has been priced-in across many software companies given the choppy environment, and the reward-to-risk is attractive. However, it is worth highlighting that not every software company with AI initiatives will be beneficiaries. Stock selection will be key in this phase of the cycle as we expect more dispersion as AI impacts different segments of software differently.

Top Contributors

Our underweight position in technology hardware producer Apple Inc was a top relative contributor due to its significant weighting in the benchmark. Apple had an average 11.5% weight in the benchmark, while the fund had an average weight of 1.1%. Shares pulled back earlier in the year on softer iPhone shipments in China and from the EU commission issuing a fine on Apple. Also, the Fund reinitiated a position in April, capturing the stock’s rally into and following Apple’s Worldwide Developers Conference in June.

Social media operator Meta Platforms was among the top contributors. Shares were higher as the company continued to deliver strong earnings results helped by better-than-expected revenues. Meta’s “year of efficiency” continues as expenses remain controlled, translating to operating margin expansion and higher overall net income. The company is working on new ways that generative AI can improve experiences across Facebook, Instagram, Messenger and WhatsApp—spanning search, social discovery, ads, messaging and more. This includes a Generative AI personal assistant with robust functionality that rivals other co-pilot AI applications. We believe these new innovations can help drive greater user engagement and stickiness, as well as improvements with ad targeting and monetization.

Top Detractors

NVIDIA was among the largest overall relative detractors over the year-to-date period. Although the stock was a meaningful position in the Fund, we had a relative underweight positioning. The custom benchmark had an average allocation of 8.5% and ended the half year period at 11.0%, while the Fund averaged a 4.5% weight. Shares of NVIDIA rose 149% over the period as the company consistently delivered better-than-expected earnings results, as demand continues to out-strip supply. New product announcements were also constructive for shares, including the new Blackwell GPU architecture. Although we opportunistically took profits, we still favour the stock as one piece of a diversified exposure to the AI infrastructure opportunity.

Our position in electric vehicle (EV) maker, Tesla, was also a top detractor. Shares underperformed from January to mid-April, as EV demand broadly decelerated and amid uncertainty surrounding Tesla’s vehicle price cuts. However, prior to releasing earnings results in April, we added to the position as we believed there was a misunderstanding on the transitory nature of the company’s lower production and delivery numbers. Shares rallied following Q1 earnings results, as management announced an accelerated timeline for a mass-market vehicle and guided to a recovery in production for the rest of the year. This slightly offset the share price weakness from earlier in the year. Looking forward, Tesla has some of the most ambitious innovation agendas of most any public company, spanning electric vehicles, energy transition, artificial intelligence, and advanced robotics. We believe the company is making strong progress on each of these agendas in ways that can unlock significant shareholder value in the future.

Notable Portfolio Changes

During Q2 2024 period, we made some shifts to align the portfolio with our highest conviction ideas with attractive upside potential. From a buy perspective, we adjusted our AI infrastructure holdings to increase exposure to companies that have underappreciated earnings upside from the strong AI investment backdrop and should also benefit from a market broadening. This includes new positions in Dell Technologies, which is a leading supplier of AI servers and services, and in Oracle, an enterprise software provider with a cloud business that is experiencing an inflection in customer demand for AI workloads. We also increased our position in Broadcom, as the company continues to win new designs for custom AI chips and is positioned for a broad-based semiconductors recovery. Within AI Applications, we also opportunistically re-initiated a position in cybersecurity provider Zscaler, as valuations reached an attractive level while the company continues to innovate products and introduce more AI capabilities. Also, we reinitiated a position in Apple in April as we believe reward to risk reached an attractive level given prior share price underperformance and that investors were underappreciating the upside potential from the introduction of AI into the Apple’s ecosystem.

Regarding larger portfolio sells, we were focused on adjusting positions where risk reward became more balanced. We trimmed our AI Infrastructure position in internet search and advertising provider Alphabet following better-than-expected earnings results. Within AI-enabled Industries, we also lowered our exposures to solar inverter company Enphase on nearterm policy uncertainty. We also reduced energy services provider Schlumberger, given a potential digestion period as investors get comfortable with the newly announced ChampionX acquisition. We also took profits in copper producer Freeport McMoRan and in DexCom, which provides continuous glucose monitoring medical devices.

Message to Investors

To our investors, we are grateful for your continued support and trust as we navigate this period of transformation. While 2023 was a robust year, 2024 has so far been difficult from a relative performance perspective. Simply put, this was an outcome that has not met the high standards we set for ourselves. The fund was early in positioning for a market broadening outside the technology giants and an upcoming wave of AI applications. However, from our bottom-up research, our conviction remains high on these trends eventually playing out. In these times of technological advancement and shifting market dynamics, it is crucial to invest not based on yesterday’s winners but on how the landscape evolves. An environment characterized by disruption and change will create significant opportunities for stock selection, especially in areas with market skepticism. Right now, markets are likely misunderstanding the upcoming broadening that expands from AI Infrastructure to AI Applications and AI-enabled Industries.

As we have done since the launch of the strategy in 2016, we remain focused on identifying the companies that leverage AI to deliver the most shareholder value creation over the long term. Relative to the technological advancements that lie ahead, we are still at the very beginnings of the AI revolution.

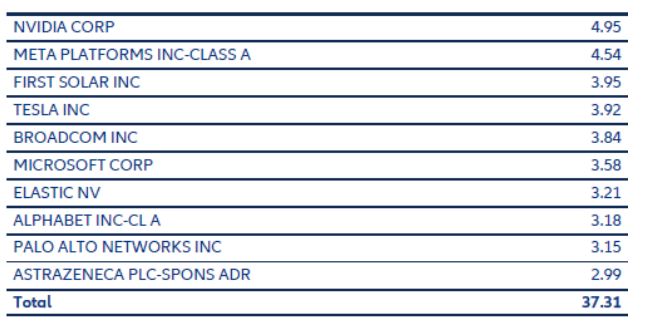

Top holdings in %

End of June 2024. This is for guidance only and not indicative of future allocation. Securities mentioned in this document are for illustrative purposes only and do not constitute a recommendation or solicitation to buy or sell any particular security. These securities will not necessarily be comprised in the portfolio by the time this document is disclosed or at any other subsequent date.

Diversification does not guarantee a profit or protect against losses.

This is not a recommendation or solicitation to buy or sell any particular security or strategy.