The following content has been prepared by Allianz Global Investors GmbH (AllianzGI), and is reproduced with permission by Voya Investment Management (Voya IM). Certain information may be received from sources Voya IM considers reliable; Voya IM does not represent that such information is accurate or complete. Any opinions expressed herein are subject to change. Nothing contained herein should be construed as (i) an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security.

The following content has been prepared by Allianz Global Investors GmbH (AllianzGI), and is reproduced with permission by Voya Investment Management (Voya IM). Certain information may be received from sources Voya IM considers reliable; Voya IM does not represent that such information is accurate or complete. Any opinions expressed herein are subject to change. Nothing contained herein should be construed as (i) an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security.

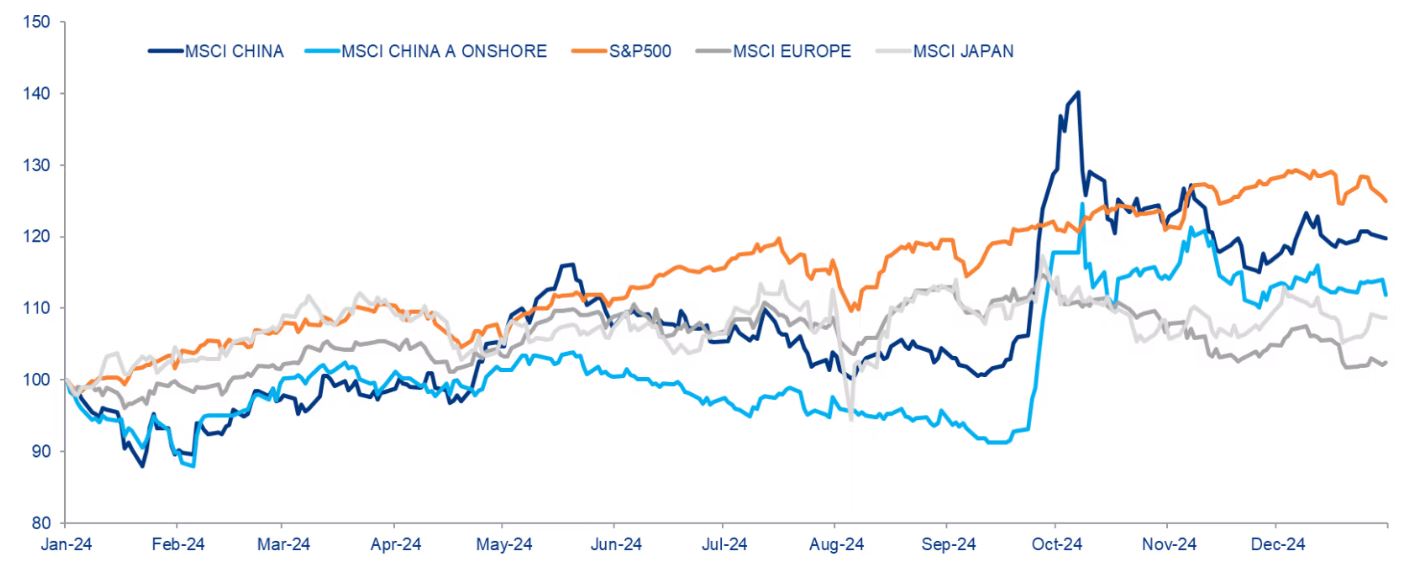

It’s fair to say it has not had the feel of a bull market.

Please find below our latest thoughts on China:

- China equities ended the year with double-digit gains in US dollar terms in both onshore and offshore markets. This made them one of the better-performing global asset classes in 2024 and ended a three-year losing streak.1

- Despite the improved performance, it’s fair to say it has not had the feel of a bull market. Sentiment clearly remains quite muted.

- Partly that’s because the China A market was down in eight of the 12 months of last year. And most of the gains occurred in a relatively short period towards the end of September and into October, spurred by a significant change in government policy.2

- There’s an important takeaway for global asset allocators. In this policy-driven environment where timing is unpredictable, if you don’t already have some exposure to China equities it may be very hard to react in time and catch the rally. Or as the saying goes, you have to be in it to win it.

Chart 1: 2024 performance of major stock market indices (USD, rebased to 100)

Source: LSEG Datastream, Allianz Global Investors, as at 31 December 2024.

- Before looking ahead to the upcoming Chinese New Year of the Snake, a quick word on the weaker market performance in the early days of January.

- While this is partly due to the strength of the US dollar and rising bond yields globally, which have impacted most of the emerging market universe, the first two months of the calendar year are also frequently quite turbulent in Chinese markets.

- A key factor is the pause in policy announcements and a vacuum in macro data availability. Because of the Chinese New Year holiday, which falls either in late January or early February depending on the lunar cycle, economic statistics for the first two months are combined and only announced in mid-March.

- The economic policy news cycle goes into a similar lull. Important details such as the country’s annual GDP target and government budget are not announced until the annual meeting of the National People’s Congress in early March.

- And with the incoming Donald Trump administration promising action on tariffs from the first day in office, this year this information vacuum provides even more fuel for market volatility than usual.

- Even allowing for this geopolitical uncertainty, however – and perhaps counter to consensus thinking – overall we currently see more upside than downside risk in China equities.

Chart 2: Shanghai Composite Index, 5 years

Source: Wind, Allianz Global Investors as at 15 January 2025.

- Part of this view is based on the “Beijing put” helping to put a floor under the market.

- For some global investors, the idea that government policy can or will play such a direct role in shaping equity market dynamics can be hard to buy into. In this context, it’s important to see the situation from a local investor perspective. After all, foreign investors own only around 4% of the China A market.3

- The People’s Bank of China (PBOC) sent a strong signal last year that it is willing to act as the lender of last resort to backstop the market by extending significant amounts of credit for stock repurchases, which already reached a record high level in the China A market last year.

- Looking ahead, the establishment of a national stabilisation fund would provide further support as a buyer of domestic ETFs.

- As such, we believe there is significant downside protection if needed for onshore markets. “National team” buying has previously kicked in around the 3,000 level on the Shanghai Composite Index – the current level is around 3,200.4

- Of course, limiting downside is one thing. Generating more sustainable gains is quite another. The experience of recent months is that “jawboning” cannot work indefinitely.

- Policymakers will need to back up their signals with further concrete measures if the sustainability of the improved economic momentum in recent months is to continue.

- Earlier this week, Beijing, Shanghai and Guangdong all announced a GDP growth target of “around 5%”. In the past, their GDP targets have been broadly in line with the national target.5

- With China’s export momentum – a key driver of growth last year – likely to fade in 2025, an improvement in domestic demand will be needed to achieve the GDP growth target.

- As such, we expect a continuation of looser monetary and more expansionary fiscal policy. This increases the likelihood of better prospects for corporate earnings, which have been a significant drag on markets in the recent past.

- Perhaps Chinese equities in the Year of the Snake are set to shed their previous skin and take on a different form.