| The following content has been prepared by Allianz Global Investors GmbH (AllianzGI), and is reproduced with permission by Voya Investment Management (Voya IM). Certain information may be received from sources Voya IM considers reliable; Voya IM does not represent that such information is accurate or complete. Any opinions expressed herein are subject to change. Nothing contained herein should be construed as (i) an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. |

By Gregor MA Hirt, Global CIO Multi Asset, Allianz Global Investors.

What has happened?

French President Emmanuel Macron called a snap general election following the success of far-right parties in the EU elections in June.

The first round of the election is to be held on 30 June followed by a final round a week later. According to the polls, the governing party – President Macron’s Renaissance – is set to lose power although the final outcome of the election is uncertain.

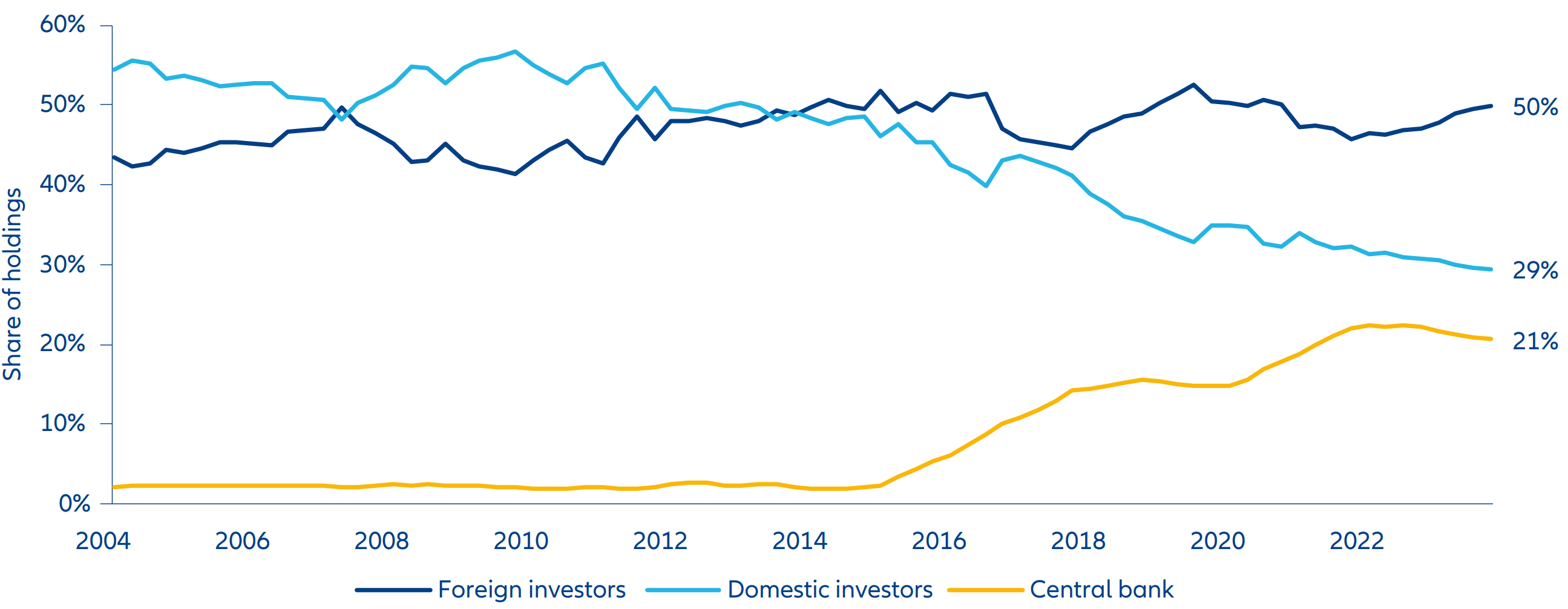

Financial markets have responded with alarm at the possibility of the far-right National Rally (RN), led by Marine Le Pen, forming a government. The euro fell for two days in a row against the dollar and the CAC 40 was down more than 6%1 in the days following the election announcement. In a reflection of the turmoil, the gap between French and German 10-year government bond yields – a barometer of risk premium on French government bonds – reached its highest point since February 2017.2 A high share of foreign holdings (see Exhibit 1) makes French government bonds vulnerable, and a further rise in spreads could have wider implications for the euro.

Source: Allianz Global Investors Global Economics & Strategy, IMF (data as of Q4 2023)

The background

Even before the announcement, rating agency Standard & Poor’s had downgraded France’s creditworthiness from AA to AA- on the back of concerns that higher than expected deficits would push up debt.

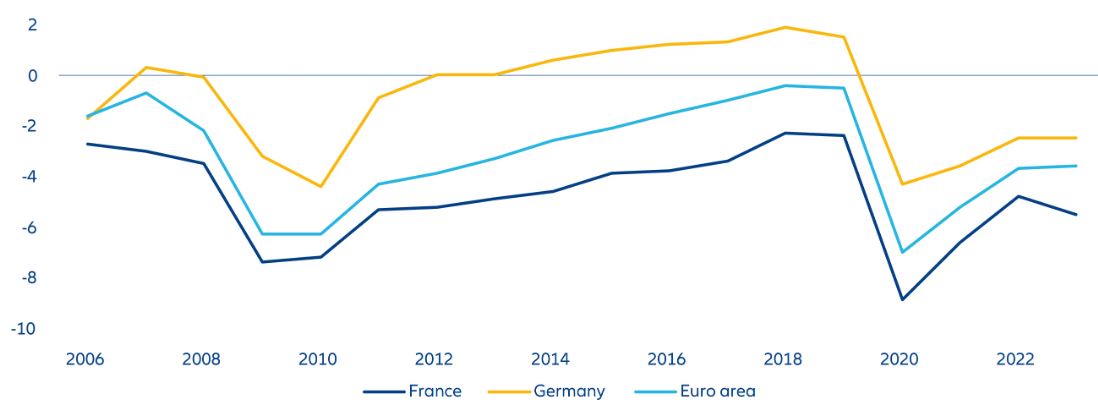

The French economy has been in the doldrums for some time and the public finances are stretched. France has consistently run a larger budget deficit than the euro area average and even more so compared with Germany (see Exhibit 2). Unlike some other euro zone countries, France did not make major reforms to its economy, particularly its labour market, during the European sovereign debt crisis of 2009-10. The prospect of a populist government seeking to raise public spending further is toxic for markets against this backdrop.

Source: AllianzGI, Bloomberg, 31 May 2024

The second challenge is that France has lagged other countries over the last decade in generating growth. Indeed, on IMF projections, GDP per capita is projected to lag the US and Germany over the coming five years. This helps explain some of the drift that Ms Le Pen's party successfully drew on in the EU elections.

What happens next?

At this stage we see three possible outcomes of the elections:

- RN wins an absolute majority of seats in the Assembly (unlikely).

- RN wins a relative majority (most likely).

- Left-wing alliance wins a relative majority (least likely).

In the first two cases, President Macron would face intense pressure to nominate a RN Prime Minister, although RN leader Jordan Bardella has said he would not take up the role without an absolute majority.

The economic policies of RN are evolving. Estimates based on the programme set out by Ms Le Pen when she ran for President in 2022 put the cost of the party’s policies at EUR 101 billion.3

The brief tenure of Liz Truss as UK Prime Minister was a reminder that governments ignore debt markets at their peril. Her package of unfunded tax cuts sparked economic turmoil. Similarly in France, there is the risk of a “Liz Truss moment”, where markets react negatively to a new, high-spending government – although the earlier UK precedent could have its virtues: the winning party could learn from it and be careful.

Indeed, RN is now planning reforms in two phases to reassure the markets at a time when France is already saddled with high levels of public debt. Some headline policies – such as the commitment to reduce the retirement age to 60 for some workers and a proposed EUR 7 billion VAT cut on household staples – may be delayed. RN may have an incentive to be seen as a moderate and responsible party to boost its chances in the 2027 presidential election.

Arguably, markets find the policies of the left-wing alliance even more alarming. These include reintroducing a wealth tax, raising income tax for the highest earners, and freezing the price of basic food items and energy.

Another worrying aspect is that France allows even a minority parliament to pass a bill without a vote via Article 49.3 of its constitution.

Against this backdrop, the risk for France is that the spread on its debt could continue to widen, with some French bonds already yielding more than lower-rated Portuguese paper. The hierarchy of European sovereign debt markets is being reordered as investors take a long hard look at the underlying fundamentals. In a worst-case scenario, France is downgraded further and struggles to attract foreign capital. Goldman Sachs has warned that the country’s national debt could reach 120% of GDP if RN win the election.

We see a risk of large institutional investors turning their back on France’s debt as their local interest rates become more attractive. This could have tectonic implications globally.

The good news: the fundamentals of French companies are sound

Meanwhile, the fundamentals of French companies are good. Access to finance has been easier since the beginning of the year but the uncertainty created by the early election has led to a French risk premium being passed on to companies. The flow of primary issues dried up in the week following President Macron’s announcement as the increase in France's spread begins to affect the cost of financing for its companies.

As for equities, the market lost in one week what it had gained since the start of the year. Some stocks (eg, tech and multinationals) remain relatively insulated from market movements due to the size of their global business. In fact, only 19% of the French index CAC 40 is dependent on the French economy. This portion generally includes smaller companies whose debt is held domestically. Their financing will be more expensive, which explains their decline on the stock market. The banking sector is also affected despite its healthy fundamentals.

In conclusion, investors should expect a higher risk premium and market volatility in France, which could potentially extend across the wider euro zone if France’s problems escalate.

In the coming weeks and months, the political cycle will dominate the newswires, and the minds of market participants. The main candidates’ political programmes will be intensely scrutinised, and the more outlandish campaign promises – especially those that would severely impact the French deficit – may lead to spikes in volatility and in spreads.

The extent and timing of this volatility is difficult to predict at this stage. But once the political situation becomes clearer, opportunities to add to French portfolios may also emerge given the robust underlying fundamentals in many instances. This should be the case especially after the first round of the elections on 7 July, with potentially attractive entry points emerging as the make-up of the government and its policies become clearer.

How does the situation affect our asset class preference?

- We still favour the US dollar – Any reminder of the European sovereign debt crisis is a red flag for many international investors. So, while euro zone data has surprised on the upside recently – compared with a weaker showing by the US – we maintain our overweight in the dollar versus the euro as a safe haven bet, profiting from positive interest rate differential.

- Equities: look across the Channel – In terms of equity markets, we see more potential in the UK. It is under-owned and exhibits low valuations, and its upcoming election should be a “non-event” compared with the turmoil elsewhere in Europe. However, notwithstanding a major escalation in France that spreads contagion to other euro zone countries, we do not underweight the region.

- Consider banks due to interest rates – We continue to like the European banking sector based on a constructive view of the euro zone economy, attractive valuations and strong revenue potential. Banks are in a sweet spot as they benefit from interest rates between 2-4% overall. There may be more volatility in the coming weeks, but longer term we remain confident about the sector’s prospects.

- Spreads to widen? – On the bond side, the widening of the 10-year BTP-Bund spread to around 150 basis points, as a consequence of the widening of the OAT-Bund spread, does not yet – in our view – justify a strong overweight. We would consider a spread of 200 basis points as potentially an attractive level at which to build long-term positions. Overall, we stick with our long 10-year US Treasury position in multi asset portfolios.

- Gold for diversification? – Gold is an obvious option during times of political and geopolitical tension. The recent retreat in prices may offer a re-entry point in an asset class with significant diversification potential in a cross-asset environment that currently offers little in the way of diversification.